Retirement once felt like a clear finish line: decades of work, then collecting a pension and enjoying your golden years. But in 2026, that line looks far more blurred. Around the world, countries are reconsidering when and how people retire, driven by longer lifespans, shrinking workforces and the mounting cost of ageing populations.

This creates a rich and complex patchwork of retirement ages — from early exits in France and Greece to extended working lives in Japan and the U.S. These differences aren’t just about policy choices; they reflect how each society values age, productivity and inter-generational balance.

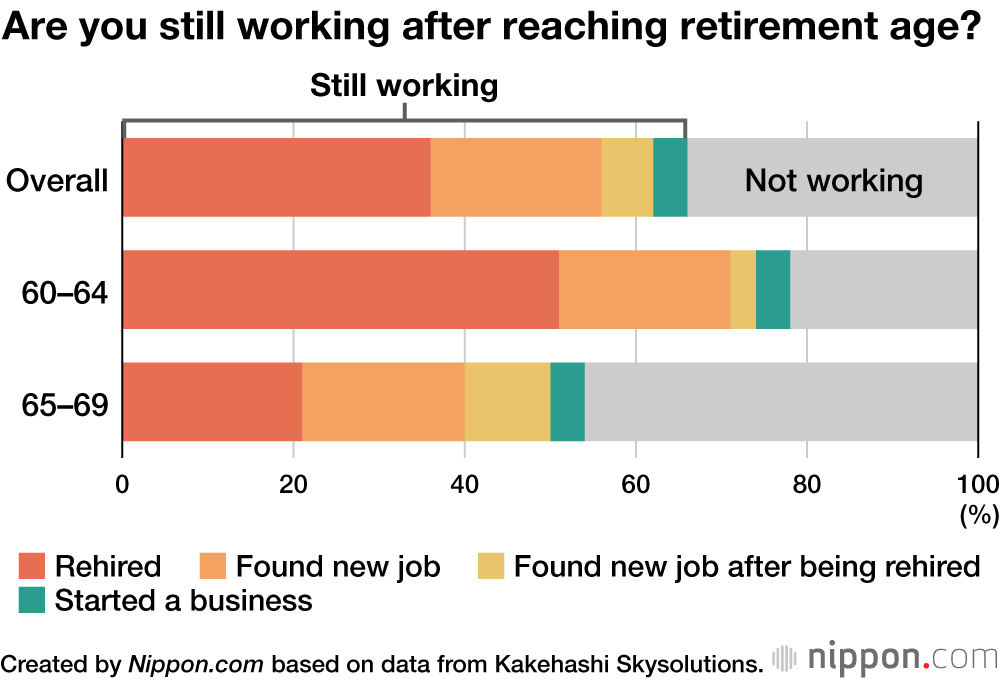

Most of the data focuses on the statutory retirement age (the age when one becomes eligible for public pension benefits), but actual working-life exit ages often diverge significantly.

According to the OECD:

To illustrate:

If someone asked: Why are so many countries increasing retirement age? — the answer has three big drivers.

The world is ageing. The ratio of workers to retirees is shrinking in most developed economies. Pension systems, healthcare and social support burdens are rising. For example, a study by the Fraser Institute noted that in OECD states, pension outlays averaged 8.2 % of GDP in 2019 and are projected to increase.

People are living longer and healthier lives, meaning the period between retiring and dying has extended — but systems built decades ago assumed much shorter retirements. The OECD paper shows that by 2050, average life expectancy past pensionable age could reach ~20.3 years for men, ~24.6 for women.

With fewer people in each working age cohort, governments and companies need older workers to stay in the game longer. Some countries are explicitly linking retirement age to life expectancy (e.g., Denmark) or incentivising delayed retirement.

Retirement isn’t just an economic or demographic issue — it’s deeply cultural.

Interestingly, many global surveys indicate that 40% of workers (globally) don’t want to fully retire; they prefer lighter, meaningful work rather than full cessation.

For HR professionals, the ageing workforce is both a challenge and an opportunity.

Older workers often bring institutional memory, mentoring capacity, and stability — but may require ergonomics adjustments, targeted training or flexible schedules.

Companies that pro-actively prepare for later retirements are doing things like:

The OECD’s research (“Is it worth raising the normal retirement age?”) shows that reforms to increase retirement age have a positive labour-market effect — but the effect is modest and delayed because of grandfathering rules.

Thus, for employers: expecting older employees to continue working isn’t as simple as just raising the age. Health, job type, flexibility, and choice play large roles.

Workforce & benefits tech is now starting to reflect the changing retirement dynamics. Platforms like Deel HR, Personio and BambooHR increasingly incorporate features such as:

For global organisations managing multi-generational workforces, these features help turn retirement from a cliff into a transition pathway.

Policy reform is often top-down (government sets age increases), but corporate strategy also plays a major role:

For example, legislation in several countries now links retirement age to life expectancy (Denmark plans age 70 by 2040).

Retirement as we knew it a fixed age, then a long rest is evolving. With populations living longer, workers staying healthier, and skill sets needing constant refresh, the picture is of transition, not termination.

High-income nations reference the OECD: raising retirement ages, linking eligibility to life expectancy, and redesigning work for older age cohorts.

For HR leaders and organizational strategists, the key message is simple: it’s not just to extend working life, but to redesign it - aligning jobs, learning, health, and benefits so that later-life work is productive, purposeful, and respectful of human difference.

In the end, retiring is no longer about leaving the workforce. It’s about continuing in it differently.

.svg)